Money, at some basic level, is just data.

In a world where more than 90% of data in the world today has been created in the last two years (1), the Fintech industry sector is increasingly showing the importance of data as a driver of disintermediation within banking by developing new tailored products & services, often via novel channels that are embedded in smart technology (e.g. smartphones & watches) and social networks.

The author has recent experience in commercialisation of Big Data, having recently exited a start-up (SIG Group), which focused on value capture in Infrastructure. Similarly, data is providing an opportunity for banks, beyond simple financial reporting and MIS by increasing the speed and means of delivering enhanced services and products such as robo-advice and live chat analytics, allowing nimbler responses to issues and product development.

The financial industry has been challenged over the past several years, with the pressures on Capex/Opex reduction or outsourcing in order to achieve efficiencies and offset the cost of greater regulation and low margin environment. Customers are also becoming increasingly aware of how their data is being commoditised and its intrinsic financial value and want greater control over its use. Banks are also trying to keep up with customers increasing interconnectivity and come to terms with technologies that are transforming other sectors from taxis to hotels to telecoms. Customers increasingly want frictionless, convenient and personalised experiences and sometimes cannot comprehend why they’re unable to perform certain tasks on their Banking App; or simply why their bank asks them for information again and again ‘when they hold the data’.

Increasingly, companies who effectively utilise intangible assets such as Data, see higher enterprise valuations, Amazon is an excellent example of this (2). This provides an advantage (and perhaps some respite) for incumbent institutions which hold vast amounts of consumer data, by providing another lever to help drive value (and ultimately share price) and commercial advantage.

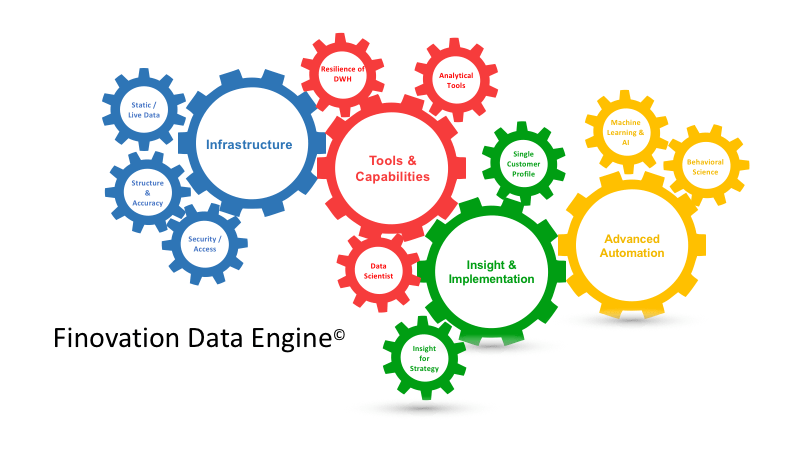

This blog post covers data at a high level and will introduce several themes and the Finovation Data Engine (Exhibit 1), which we will explore in detail in subsequent posts.

The financial services industry is, fundamentally, powered by data: this ranges from data on what available funds may be in a customer’s account, to data that helps validate someone’s identity in money laundering checks.

We are seeing several exciting themes emerge in data:

- New Battlegrounds: large consumer ecosystems (such as Apple, Facebook, Amazon and Google) hold vast amounts of data which can be used to gain insights on behaviour and help drive decisions and delivery of products. Increasingly, live and static data is being merged in the offline world (3)… what’s to stop ApplePay becoming a fully-fledged Finco by not just moving money but also providing credit.

- Relationships: Previously, incumbent institutions with vast distribution (Branches, call centres) would drown new entrants. The ability to deliver through new channels, access non-traditional data, allows challengers to scale faster and reduces the barriers to entry by allowing significant numbers of customer to engage via smart technology for highly personalised products/services quickly and easily.

- Assessing Risk: Smart new ways of assessing risk. Start-ups gobble up information, on everything from social-media reviews to companies’ usage of logistics firms, to assess how well small businesses are doing. Companies like Avant (4) use machine learning to underwrite consumers whose credit scores were damaged during the financial crisis. Augmenting traditional credit history with non-standard information is helping open up consumer credit markets, driving up competition amongst lenders.

- 360 Customer: By collecting, storing, organising and driving insight from data. Data nimble organisations can understand their customers much more effectively and more importantly drive Next Best Action from cross sell of products or services, when a customer needs them, and by the channel, be it a mobile app, web pop or Facebook message. Indeed, many organisations still to this day have challenges with answering a simple MIS questions, with their respective marketing, finance and risk departments sometimes providing different answers to same questions, primarily due to different pools of data and effective data organisation. External organisations are increasingly stepping into this gap to help provide insight from large and complex data stores (5), this in itself raises consent and data privacy questions.

- Intermediaries: Many Fintechs or challenger banks such as Tandem are taking advantage of regulations such as PSD2, which allow them to hook into or access data from larger incumbent players via API’s, driving insights for customers based on their spending behaviour across multiple dimensions – merchants, accounts and transaction types. This intermediary platform role allows a powerful profiling of customers and hence offering a clearer understanding of their need for further products or services in a highly personable and (to the customer) attractive way. At a more fundamental level, these insights improve the relationship customers have with their money. Indeed, Fintechs such as Centralway Numbrs (centralway.com/de/) are taking this a step further and creating an online banking store, allowing customers a one stop shop to purchase products from different banking providers.

The complexity and scale of a comprehensive data strategy means legacy banks can oft afford such large-scale investment with uncertain payback periods for back end transformation, large data warehouses or cloud infrastructure. In the Finovation Data Engine (Exhibit 1), we highlight how interlinked the different components of data architecture and how difficult it is to pick and choose aspects for success.

However, smaller nimbler banks can provide perspectives on a way forward, an example is CBW Bank (6) in the US, which opened its doors to partners via 500 API’s. one of its partners can decision a loan in 30 seconds and disburse nearly instantaneously… a glimmer of hope. Customers often choose banks and institutions based on how quickly transactions or payments can take and transfer and application for new products… an effective data strategy can help reduce this friction. Think, in your organisation how long does it take for an existing customer to apply for a new product or make a money transfer… then benchmark with the likes of PayPal or new Fintechs in your geography, the results will most likely surprise you !

In future posts we will be exploring the themes above in greater depth and also aspects of the Fintech Data Engine (Exhibit 1).

The key takeaway from this post is that any Fintech or Digital strategy is prone to failure if not built on an effective data strategy… increasingly Data is the fuel that drives not just Fintech but Financial Services success !

What are your thoughts ? Please share in the comments below or drop us a note.

All good things

MN

References:

- for 90% of world data Petter Bae Brandtzæg of SINTEF ICT https://www.sciencedaily.com/releases/2013/05/130522085217.htm

- com: Inside Europe’s biggest data visualisation laboratory https://www.ft.com/content/a8d9f1ca-154a-11e7-80f4-13e067d5072c

Great insight and proof that harnessing Data is the Holy grail .

Couple of observations

1- Yes Fintechs are making waves with API plug ins to approve loans in shorter timeframes but they still don’t have the ” Trust ” factor that Banks illogically enjoy .

Time and the continued commoditization of Financial services will eat into this barrier to disruption and millinials will make decisions about where to remit / borrow or hold their funds more on user views and likes – more data – then any generational nostalgia for legacy Banks.

2- Regulation in emerging markets is a short to medium term buffer for emerging market Banks to play catchup to get to a 360 view of the customer and drive real time marketing – given data is top of all transformational spend across Banks today

3- Data will transform into a new Boardroom agendas in the next two years – this is ” Digital Identity and it’s commoditization ” — this is what Google and Amazon have already got nailed down.

Again more data !

LikeLike

Great article, thanks for sharing the insight.

LikeLike